Business inventories and sales represent the beating heart of any thriving organization, directly influencing profitability and growth. Understanding how inventories are managed and how sales are tracked is essential for ensuring products are available for customers when needed and for maximizing revenue opportunities. This topic offers practical insights into how these two critical areas work together to drive business success.

From the definition and importance of inventories and sales to the advanced tools and strategies used by modern companies, the journey explores inventory components, management methods like FIFO and LIFO, key performance indicators for measuring sales, and the direct relationship between stock levels and sales outcomes. Real-world examples and case studies add valuable perspective, making the topic both relevant and actionable for business owners, managers, and anyone interested in the mechanics of commerce.

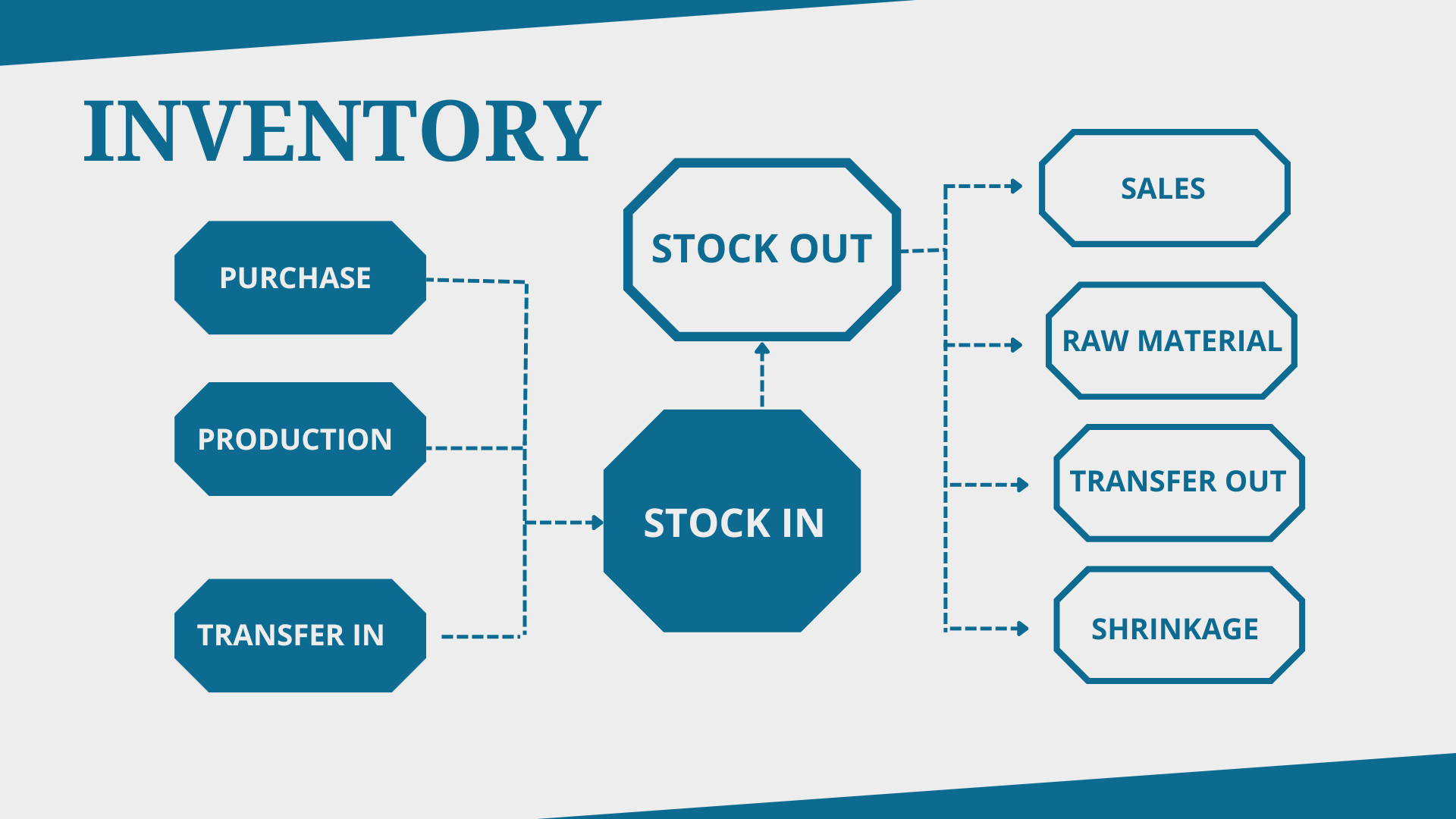

Business Inventories and Sales: Definition and Importance

Business inventories and sales are fundamental concepts in the commercial world, shaping the core of every organization’s operational and financial health. Understanding what they mean, their roles, and their broader economic significance lays the groundwork for efficient day-to-day operations and strategic planning.

In a commercial context, business inventories refer to the goods and materials a company holds for the purpose of resale or production. These inventories can include raw materials, items currently being processed, and finished products ready for sale. Sales, on the other hand, represent the process and outcome of selling these goods or services to customers, directly driving revenue and business sustainability.

Inventories and sales are interconnected elements in business operations. Inventories ensure businesses can meet customer demand without delay, while sales convert those inventories into profit. Effective inventory management helps maintain a balance between having enough stock to satisfy demand and avoiding excessive surplus that ties up capital.

From an economic standpoint, accurately tracking inventories and sales provides organizations with crucial insight into consumer demand, production efficiency, and cash flow management. These metrics inform decisions on purchasing, pricing, logistics, and even future business expansion.

A clothing retailer that closely tracks its inventory knows exactly when popular items are running low and can reorder in time to avoid stockouts. This responsiveness boosts customer satisfaction and drives higher sales, while poor inventory management can lead to missed sales opportunities and excess stock that may require discounted clearance.

Components of Business Inventories

Business inventories are categorized into distinct types that reflect their stage within the production or sales cycle. Understanding these components is critical for effective inventory management and accurate business reporting.

There are three primary components of business inventories:

- Raw Materials: Basic inputs purchased to be used in the production process.

- Work-in-Progress (WIP): Items currently undergoing transformation during the manufacturing process.

- Finished Goods: Products that are completed and ready for sale to customers.

The table below organizes examples of each inventory type to clarify their distinctions and practical implications:

| Inventory Type | Example | Description |

|---|---|---|

| Raw Materials | Steel bars at an auto parts factory | Essential materials acquired to produce car components, not yet altered from their original state. |

| Work-in-Progress | Partially assembled smartphones | Products in various stages of assembly, not yet ready for market release. |

| Finished Goods | Bottled beverages at a distribution warehouse | Completely manufactured products awaiting shipment to retailers or customers. |

Accurate categorization of inventories not only improves internal tracking but also ensures transparent financial reporting. Businesses must report inventory values in their financial statements, and clear distinctions between inventory types support compliance with accounting standards and facilitate better strategic planning.

Methods of Inventory Management: Business Inventories And Sales

The choice of inventory management method impacts a company’s operational efficiency, cost structure, and responsiveness to market demand. Several recognized approaches are employed across industries, each with unique advantages and limitations.

Common inventory management methods include:

- FIFO (First-In, First-Out): The first items added to inventory are the first sold or used, typically mirroring the chronological order of stock movement.

- LIFO (Last-In, First-Out): The most recently acquired items are sold or used first, which can affect tax liability and profit reporting.

- Just-in-Time (JIT): Inventory is kept minimal and materials are ordered only as needed for immediate production or sales, reducing holding costs.

A comparative overview of these methods is provided below:

| Method | Advantages | Disadvantages | Typical Industry Usage |

|---|---|---|---|

| FIFO | Reflects actual physical flow, reduces spoilage, higher reported profits in inflationary times | Higher taxes in inflation, may mismatch current costs with current revenues | Food and beverage, pharmaceuticals, perishable goods |

| LIFO | Lower taxes in inflation, matches recent costs to current revenues | Banned under IFRS, higher risk of old stock obsolescence | Some US retailers and wholesalers, raw material-heavy industries |

| Just-in-Time | Minimizes holding costs, increases efficiency, responsive to market changes | Risk of supply chain disruptions, requires accurate demand forecasting | Automotive manufacturing, electronics, fast fashion |

Inventory management approach directly influences sales efficiency. For instance, JIT reduces excess inventory, freeing up cash and storage space, but demands precise sales data and reliable suppliers. In contrast, FIFO and LIFO affect profitability and risk differently, potentially impacting pricing strategy and customer availability.

Measuring Sales Performance

Assessing the effectiveness of sales activities is essential for optimizing business growth, setting targets, and aligning inventory decisions with market demand. Several techniques and indicators are used to monitor sales performance.

Sales performance is often measured using both quantitative and qualitative metrics that provide actionable insights into a business’s sales cycle, customer engagement, and overall success.

Key performance indicators (KPIs) related to sales include:

- Total revenue generated within a period

- Sales growth rate compared to previous periods

- Average transaction value

- Conversion rate from leads to sales

- Number of new and repeat customers

- Gross profit margin on sales

- Sales per employee or sales representative

Analyzing sales data enables businesses to make informed decisions regarding inventory purchasing, production levels, and forecasting. For example, identifying seasonal spikes in sales can prompt increased inventory buildup before peak periods, while slow-moving items might trigger promotional campaigns or inventory reduction strategies.

Relationship Between Inventories and Sales

Inventory levels are closely linked to sales outcomes. Balancing inventory avoids the pitfalls of both overstocked and understocked situations, which can directly impact revenue, customer satisfaction, and operational costs.

Maintaining the right amount of inventory ensures that businesses can promptly meet customer demand, while excess inventory can strain cash flow and lead to markdowns. Insufficient inventory, in contrast, may result in lost sales and diminished brand reputation.

Here are common scenarios illustrating these relationships:

| Scenario | Inventory Status | Sales Impact | Business Response |

|---|---|---|---|

| High demand for a new product | Insufficient stock | Missed sales opportunities, potential customer loss | Expedite restocking, improve demand forecasting |

| Overestimation of seasonal demand | Excess inventory | Need for discounts, increased holding costs | Seasonal promotions, adjust future order quantities |

| Accurate demand forecasting | Optimal inventory | Consistent sales, high customer satisfaction | Maintain forecasting system, continuous monitoring |

Effective management of inventory in relation to sales performance is crucial for maximizing business revenue and maintaining a competitive edge.

Ultimate Conclusion

In summary, mastering business inventories and sales is a game-changer for any company looking to enhance efficiency, profitability, and customer satisfaction. By adopting effective management methods, leveraging technology, and understanding the interplay between inventory and sales, businesses can stay ahead of challenges and seize opportunities for sustainable growth.

Question Bank

What are business inventories and sales?

Business inventories refer to the goods and materials a company holds for the purpose of resale or production, while sales represent the transactions where these goods or services are exchanged for payment.

Why is inventory management important for sales?

Effective inventory management ensures that products are available to meet customer demand, prevents stockouts or overstocking, and helps maintain a steady flow of sales and revenue.

How do inventory levels impact business revenue?

Too much inventory can tie up capital and increase costs, while too little can lead to missed sales opportunities and dissatisfied customers, both of which affect overall revenue.

What technologies can help manage inventories and sales?

Technologies like ERP systems, point-of-sale software, and inventory tracking tools streamline processes, improve accuracy, and enhance real-time decision-making in inventory and sales management.

How often should inventory and sales reports be updated?

Reporting frequency varies by business, but many companies update inventory and sales reports weekly or monthly to stay informed and responsive to market changes.